Your education is a great investment. Start managing that investment now by acquiring money management skills that will help you make sound financial decisions.

Financial wellness appointments

Have questions about money? One Stop counselors are certified in personal financial management and are here to help you. Some examples of the topics certified One Stop counselors can help you with:

- Student/personal loan debt management

- Creating a spending plan

- Understanding credit

- Setting financial goals

If you’d like to set up a 30-45 minute, 1:1 meeting with a certified One Stop counselor, simply send an email with what you would like to discuss from your University of Minnesota email account to [email protected] with “Financial wellness appointment” in the subject line.

A counselor will be in touch to set up an appointment and will then pull together specific resources to customize your meeting. We’re here to help you with your questions, not tell you what to do.

Financial Wellness

Budgeting and Spending

A budget is an itemized list of income and expenses within a set period of time. It can be used as a personal guide on what money you have coming in and where it goes when it is spent. Because a budget shows the ebb and flow of your money, it can also help inform changes you would like to make to your spending habits in order to meet financial goals. No matter how much money you make, a budget can help you manage your spending and reach financial goals.

If you’d like to meet with a financial wellness counselor in One Stop Student Services to talk about budgeting specific to your needs, schedule an appointment.

Choose a budgeting method

A budget is often created and managed in a spreadsheet, but there are many ways to do it. It’s all about finding a system that works for you. The way you keep your budget should be feasible for everyday life, manageable enough for you to want to keep up with it, and fluid enough that it can accurately reflect your income and expenses on a daily basis.

Before you start to do the hard work of tracking your income and expenses to create a budget, determine what style of budgeting will work for you. This may take some research or experimentation. Even if you decide today to budget one way, you can always change your plan later. Here are some common methods of budgeting:

- Paper and pen: collect receipts and record expenses.

- Excel sheet: track expenses using columns and rows in a way that works for you.

- Online budget sites/apps: do a Google search to see what’s out there. Many sites have matching apps that work for budgeting on the go.

- Envelope method: have an envelope for each of your expenses and insert cash in each envelope to track how much money you have for each expense.

Create a budget

The basic principles of budgeting remain the same no matter what budgeting method you choose:

Step 1: Develop your financial goals

What financial goals are important to you? Do you want to minimize your school debt? Do you want to save for a car or vacation? Putting money aside can be hard, but determining your financial goals can make it easier. When setting a goal, use the SMART method; you want goals that are Specific, Measurable, Achievable, Relevant, and Time-based.

For example, imagine that you have used public transportation on campus and enjoyed saving money by not owning a car. But things will change, and you know you want to buy a car after you graduate. After doing some research, you decide you would like at least $2,500 for a down payment on a loan for a car. You have 36 months to save for your goal before you graduate, so that means you need to save $70 a month to meet your goal. Here is the breakdown of this scenario as a SMART goal:

- Specific: Buy a car after you graduate.

- Measurable: Have at least $2,500 for a down payment.

- Achievable: Save $70 a month.

- Relevant: You are passionate about the goal because you want to enjoy the freedom of a car for transportation.

- Time-based: Reach your goal in 36 months, or three years.

Step 2: Calculate your income

Income is money that you receive, whether it is earned, gifted, or loaned to you. Income may arrive in a lump sum, such as from a financial aid refund, or it may come to you regularly through a job or allowance.

You may already know how much money you receive and when, but it is conventional to think of income on a monthly basis. If, for example, you receive a financial aid refund at the beginning of the semester that you want to last through the end of the semester, divide the lump sum by the number of months to determine how much monthly income it provides you. If you receive a refund of $1,200 and you want it to use it over a three-month period, it provides $400 per month. Determine what your income is on a month-to-month basis.

Step 3: Calculate your expenses

An expense is the cost of something. Your expenses are the money you spend, both on items expected and not expected such as rent, bills, subscriptions, groceries, clothes, fun money, gifts, etc. Even savings or financial goals are expenses, even though the actual spending is slightly more delayed in time. Think of your expenses as existing in three different categories:

- Fixed needs: necessary expenses that stay the same each month (i.e. rent, phone bill, loan repayment)

- Variable needs: necessary expenses that vary from month to month (i.e. food, clothes, transportation)

- Wants: nonessential expenses (i.e. dining out, entertainment, coffee)

The best way to start tracking and categorizing your expenses is to check your previous bank statements. You can also start tracking your receipts to build a list of expenses if you do not have your own bank account. How you track your expenses should be driven by your method of budgeting.

Step 4: Analyze your income and expenses against your financial goals to make spending decisions

As you map out your income and expenses, you’ll start to get an idea of how your financial goals are affected. You may want to make decisions about spending in order to prioritize a financial goal, or to start building savings, create an expense category in your budget for it.

If you find that you have a surplus of income, determine how you want to spend that money. If your expenses are greater than your income, find items in your budget that are nonessential. You can cut out certain expenses until you reach a savings goal, or set fixed limits for yourself in certain categories.

Be easy on yourself as you begin living by a budget and changing your spending habits. Ultimately, a budget can empower you and give you control over your money. Training your brain to practice financial wellness will benefit you now and well into the future.

Additional resources

- S.M.A.R.T Goals Worksheet (pdf)

- Net Worth Statement (pdf)

- Spending Plan Worksheet (pdf)

- Tips on tracking expenses (article)

- Budgeting apps for college students (article)

- How to build a budget (article)

- Free budgeting tools (article)

- Effective U: Learn more about managing your money

Loans and Repayment

Many students take out loans over the course of their academic careers to help pay for the cost of college. Determining what and when to borrow is an individual process.

After you apply for financial aid, the Office of Student Finance (OSF) sends a financial aid package to offer you financial aid for which you are eligible. Financial aid packages may include grants, scholarships, work-study funds, and/or loans. When you receive your financial aid package, you can decide to accept or decline any parts of the aid. Read the information below to learn more about borrowing, or contact One Stop Student Services for assistance.

Deciding what to borrow

Borrowing money for college is an investment that impacts your future finances. Any loan taken out today will need to be repaid after you graduate, and the greater your total borrowing, the greater your payments will be post-graduation.

You are not required to borrow all of the loans or loan amounts offered to you. You can decline or accept a loan, and you can decrease the amount of a loan you would like to borrow. We recommend that you borrow only what you need to minimize your overall debt.

Here are some tips to help you evaluate when and what to borrow:

- Consider your cost of attendance for the upcoming year (tuition, fees, books, supplies, etc.).

- Create a budget to track spending and plan for costs.

- Track your previous borrowing history through the Direct Loans website. Note that this site has a record of only your Direct Loan borrowing.

- Compare terms and rates of loans you are considering. Not all loans offered may meet your needs.

- Use a Direct Loan repayment estimator to calculate what your future payments may be.

Repayment after you borrow

Repayment

If you take out loans while in school, your loan service provider will send notifications of your payments when you are close to entering the repayment period post-graduation. Before your first payment is due, we recommend that you review the different types of repayment options available. You can get this information from your loan service provider.

Loan consolidation

Loan consolidation is a process that pays off each of your individual loans and rolls them into one, combined total that has one monthly payment and a single interest rate. Consolidation is available for many types of loans including both student and private. Note that federal consolidation is only available for Direct Loans. If you choose to consolidate, be aware of the terms and conditions of the agreement. Some consolidation agreements may prevent loan forgiveness.

Deferment and forbearance

If you are having trouble making your loan payments, you can contact your loan service provider to talk about alternatives such as payment deferment or forbearance. In many cases, your servicer will request documentation from you to verify your current financial situation, and from there can help determine the best option available. You may be able to switch to an income-based repayment plan, or qualify for a deferment or forbearance on your loan and interest payments due to financial hardship.

Additional resources

- Federal Direct Loans

- Federal student aid glossary of terms

- Undergraduate loan comparison chart

- Graduate loan comparison chart

- Federal student loan repayment estimator

- Direct Loan consolidation

- Effective U: Learn more about managing your money

- Student loan advocate: If you are a Minnesota resident and are having issues with your student loan lender or servicer, the Student Loan Advocate at the Minnesota Department of Commerce is willing to assist you. To learn more about this resource, to file a complaint, or to ask questions, go to their student loans webpage or call 651-539-1022.

Credit

Credit is the availability or access to money that you have not yet earned. In this way, credit is your ability to borrow money from a bank, lender or creditor with the promise of paying them back.

How well you meet that promise to pay back borrowed money, or your creditworthiness, is collected by private reporting agencies in your credit history and report. Banks, lenders, and creditors voluntarily report this information and it is used to calculate your credit score.

Credit scores can be used to:

- Assess your borrowing eligibility

- Determine your interest rate on loans (auto, home, etc.)

- Calculate your insurance rates

- Evaluate risk of non-payment by prospective landlords

If you’d like to meet with a financial wellness counselor in One Stop Student Services to talk about credit and your specific needs, schedule an appointment.

Tips for building good credit as a student

What can you do now to help build your credit?

- Only borrow what you need - try not to borrow any more loans than are necessary for your educational and living expenses. Keeping your debt as low as possible will positively impact your credit. If you have questions about budgeting for your loans we are here to help!

- Living off campus? Be sure to pay your rent and utilities on time! Paying bills by their due dates help build a good credit history.

- If you have a credit card try not to carry a balance. Paying off your credit balance every month will prevent you from paying interest on your charges.

- To avoid late fees, make at least the minimum payment every month. However, you will still need to pay interest on the remaining balance.

- Don’t apply for credit cards just to get a discount. Many retail stores have credit cards which will give you a discount just for applying. But, whenever someone checks your credit it negatively impacts your credit score, even if you are declined for the card. Apply for credit cards sparingly.

- If you have student loans take advantage of auto-pay once you are in repayment. You will set this up through your lender and makes sure your loans are paid on time each month.

What is a credit report?

A credit report gives your credit history, i.e. a list of your accounts (past and present) and how you manage them. The report will include, but is not limited to:

- Current balances

- Payment history

- Any past due information

- Age of accounts

A credit report is like your financial or borrowing resume.

The main purpose of a credit report is to determine if you’ll pay back what you borrow. People with bad credit can still get approved for additional credit, but most often they will have to pay more for the risk the lender is taking by loaning them money. This can lead to higher interest rates. Alternatively, good loan and debt management practices can help you build good credit, which can positively impact how lenders evaluate your credit risk.

Checking your credit report

It is recommended that you check your credit report at least once a year to ensure accuracy - be sure to report any errors immediately. This can be a good way to find previously unnoticed cases of identity theft. You are entitled to a free copy of your credit report once per year from each of the three major credit bureaus: Equifax, Experian, and TransUnion.

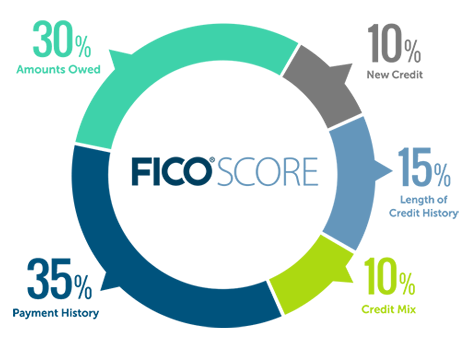

What is a credit score?

Your credit score is a snapshot in time (like your GPA), taking into account a variety of financial factors. This number is a good indicator of both your credit history and potential risk.

- 740-850: Excellent credit

- 690-739: Good credit

- 630-689: Average/fair credit

- 300-629: Bad credit

What makes up your credit score? (Chart from MyFico.com)

Using credit cards responsibly

For students, credit cards can be a convenient tool and smart usage can help you build a healthy credit score. However, credit cards can be a very destructive financial force if not used wisely. Credit cards should not be used to finance debt as credit card interest rates are among the highest.

The Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009 set new protections for credit card users. If you are under the age of 21 and want to open a credit card account, you will need to show that they can afford to make payments. Otherwise, credit card companies will require a cosigner who is 21 or older.

Pros for credit cards:

- Can help increase credit score

- More protection against fraud for purchases

- Convenience

- Pay later for purchases made now

- Automatically keeps a record of purchases - helpful for budgeting

- Good for emergencies

Cons for credit cards:

- High-interest rates

- Consequences for not paying full balance

- Impact on future loans/mortgages/car loans

- Possible hidden fees

- Easy to overspend

- Under 21 rule of credit cards (from the CARD act of 2009)

Tips for using credit cards:

- Keep track of your spending

- Stick to your budget, remember you will have to pay for your purchases later

- Set reminders to pay your bill/balance

- Make sure to read all terms carefully

- Pay your balance on time and in full each month

- Stay well under your total credit limit

Additional resources

Banking Basics

Banking is the foundation of personal finances. It is the services offered or the business conducted by a bank, a financial establishment that takes deposits, issues loans, and exchanges money on your behalf. Familiarity with banking concepts can help you navigate important decisions throughout your life. A basic checking account, and possibly a savings account, can make it easy to keep track of your finances as you earn, receive, exchange, spend, and save your money. Read more about deposits, spending, and the common types of bank accounts below. More information about budgeting and spending is also available.

If you have questions, or would like to talk with a financial wellness counselor about your specific needs, schedule a financial wellness appointment with One Stop Student Services.

Direct deposit

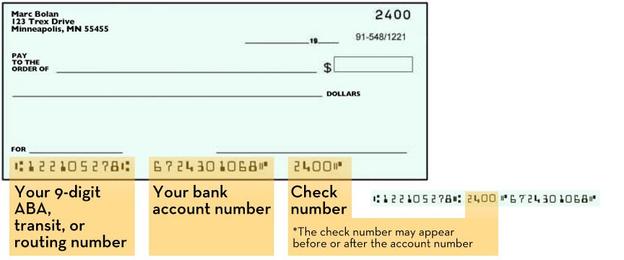

Direct deposit is a process that most banks, universities, and employers use to send funds directly to your bank account. This allows money to get to you quickly and efficiently, and eliminates the process of paper checks, which can be less secure than utilizing direct deposit. When setting up direct deposit, you will be asked to provide the account number and routing number that is provided by your bank, or found on your checks, to set up direct deposit.

Specific to being student at the University, we recommend that you set up direct deposit. This way any refund owed to you from your student account will be sent seamlessly. The University finds that students relocate fairly often; to minimize paper checks being sent to wrong addresses, direct deposit is strongly encouraged. Note that setting up a direct deposit account as a student for refunds is not the same as setting up direct deposit for earned money such as through student employment.

Types of bank accounts

Checking account

A checking account is a main account into which you deposit money and out of which charges are drawn. There should generally be enough money in your checking account for what you need to pay for without overspending (possibly incurring overdraft fees). Debit cards and checks are linked to checking accounts, and can be used to make purchases.

Savings account

A savings account is similar to a checking account, but accrues interest for the money in the account. A savings account is a little less “liquid” than a checking account, meaning it is not ideal for making a lot of transactions in a short amount of time. There may be transfer or withdrawal limits each month that prevent high transaction activity.

529 college savings plan

A 529 plan is a tax-advantaged savings plan designed to encourage saving for future college costs. How plans are structured and how to access funds from the plan varies by state, plan administrator, and the plan itself. If you already have a 529 plan, learn how to submit payments.

Money market account

A money market account is a more complex form of a savings account. It generally accrues interest at a higher rate than a savings account, but also has higher minimum balance requirement. There are more restrictions on withdrawals, so it is even less liquid than a savings account. A money market account could be used to maintain an emergency fund, but it is intended for longer-term savings, usually after a regular savings account has been funded to your satisfaction.

Certificate of Deposits (CDs)

A certificate of deposit, or CD, is another form of savings, but generally pays higher interest than a savings account. It is used when you don’t need to access your money for 6-12 months. The longer the duration of the CD, the higher amount of interest it will earn. There are penalties for taking money out of a CD early, so it is best used when you have a savings cushion already in place, or are sure you will not need access to the funds in a CD.

Saving an emergency fund

Saving is an important part of banking and overall financial goal setting. It is a practice used to set aside money in preparation for the future, to meet short and long-term goals.

Your emergency fund can be a safety net for unexpected events, such as losing income from a job, repairing your car, a medical emergency, or short-notice expenses. An emergency fund helps you avoid going into or adding to your debt, which is a benefit to your overall, long-term financial wellness. You may find that you do not currently have the financial capability to begin an emergency fund due to personal circumstances. This is understandable. It is generally good to be aware of the benefits of emergency funds, and practice putting away money in any amount when you can.

An ideal emergency fund includes enough money to cover your expected expenses for roughly three months. You can consider a three-month emergency fund a financial goal, but having some money set aside is what is most important. Additionally, your emergency fund money should be easily accessible to you so that you can obtain it exactly when you need it without being penalized for withdrawal.

Additional resources

- Net Worth Statement (pdf)

- Money market accounts (article)

- Credit union vs. banks (article)

- How to choose a savings account (video)

- Rockstar Finance (tool)

- Effective U: Learn more about managing your money

Identity theft

Identity theft is a crime that continues to expand and affect more and more people in the United States. Identity thieves steal personal information such as name, date of birth, social security number, bank account, credit card information and more to commit fraud. Not only do the thieves seek to steal money, they also use stolen information to file taxes or get medical services. A person will often not know their identity has been stolen until they receive mystery bills, credit collections or loan denials due to poor credit caused by the theft. However, there are many precautions that you can take to reduce your risk of identity theft.

If you think you think you’ve become the victim of identity theft, report it immediately and contact your local police department.

What to watch out for as a U of M student

Email scams (known as phishing) are a common method to trick you into visiting a fraudulent website, opening an infected document, or logging in to "validate your email account." These emails, websites, documents, or login pages may be obviously fraudulent, or they may look exactly like the University's login page. The University of Minnesota Police Department has compiled a list of the most common scams targeting the University.

The University has many tips to help you recognize and report suspicious emails.

- If you responded to an email scam or clicked on a suspicious link, immediately change your password.

- Contact the University’s technology help staff.

If you are ever unsure whether an email is legitimate or not, ask [email protected].

Types of identity theft

There are many types of identity theft and, typically, they can lead to financial consequences for victims if not caught soon enough.

- Child ID theft - particularly problematic because the theft might not be identified for years.

- Tax ID theft - the use of your social security number to file false tax returns.

- Medical ID theft - using your information to get services or file false medical claims.

- Social ID theft - someone uses your information and photos to create a fake social media platform.

Identity theft prevention

- Do not carry your social security card with you. Be very careful who you give your SSN out to. Avoid ever giving your SSN out over the phone.

- Never respond to unsolicited requests for personal information.

- Lock your cell phone and laptop, do not leave open and unattended.

- Monitor your bank accounts and credit accounts frequently. Don’t just wait for statements in the mail.

- Use complex enough passwords not containing obvious information such as date of birth.

- Order your credit report once a year.

- Purchase a service for identity theft monitoring.

- Criss-cross shred all important documents. Don’t just discard in the trash.

Reporting identity theft

Victims of identity theft need to report the crime immediately. The two places to report your identity theft first is to the Federal Trade Commission and your local police department. After you file your report with the FTC you will receive an identity theft affidavit. Once you have this document, then you can proceed to file a report with your local police department. Your identity theft report will be critical to have when you take the next steps to notify your bank, creditors and any organization you might have a financial relationship with.